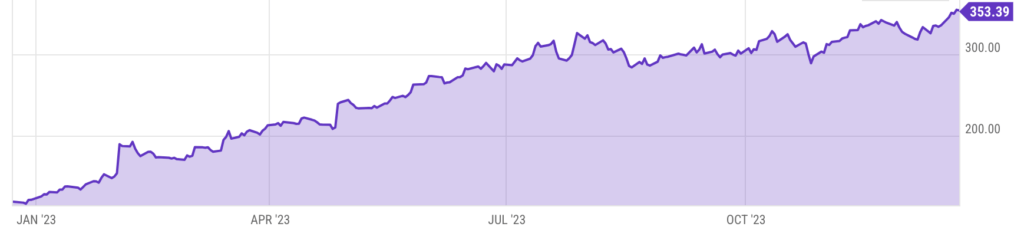

Meta Platforms (NASDAQ:META) has experienced a remarkable 187.73% year-to-date surge, showcasing a notable recovery from its $90 low at the end of 2022.

Meta’s all-time high was around $380, indicating a decline of approximately 76% to its $90 low. The reason for this substantial drop, in my opinion, can be attributed to four factors.

1. Privacy concerns

2. Reality Labs spending

3. Competition from TikTok

4. Apple’s ad targeting restrictions

Initially, I will delve into these four factors and subsequently present arguments highlighting why these issues pose no significant challenges for Meta.

1. Privacy concerns

Meta has been facing significant scrutiny and criticism over its handling of user data and privacy practices for many years now. Recently in May 2023, Meta was fined a staggering € 1.2 billion ($1.3 billion) by the Irish Data Protection Commissioner (DPC), which was the largest fine ever under the EU’s General Data Protection Regulation (GDPR). This fine emphasized the gravity of Meta’s GDPR violations, specifically the inadequate protection of EU user data transferred to US servers. The DPC found that Meta had violated the GDPR by transferring the personal data of EU users to servers in the United States without adequate safeguards in place. In addition to the hefty fine, the DPC ordered Meta to cease transferring the personal data of EU users to the United States within six months and ordered Meta to bring its data transfers into compliance with the GDPR. The fine was a consequence of Meta’s failure to adhere to a 2020 decision of the ECJ (European Court of Justice), which determined that Meta’s transatlantic data transfers (EU-US Privacy Shield agreement) lacked adequate protection from American Intelligence agencies.

While a billion-dollar fine could bankrupt most companies, the weighty fine has not significantly impacted Meta’s share value. Investor confidence appears unshaken, likely bolstered by Meta’s considerable financial reserve. As of the announcement of the fine, Meta had $37.44 billion in cash and equivalents, indicating a robust financial position that may have alleviated concerns about the penalty affecting the company’s overall financial stability. It’s noteworthy that Meta’s free cash flow was $7.16 billion in Q2 2023.

Meta’s CFO, Susan Li, informed investors that roughly 10% of the global ad revenue came from ads targeting users within the European Union. According to their earnings report of Q2 2023, their ad revenue from EU users was actually $25.33 billion in the year 2022. To put this into context, Meta’s total revenue for 2022 amounted to nearly $117 billion. This meant that not 10% but almost 22% of Meta’s global ad revenue is generated in the European Union.

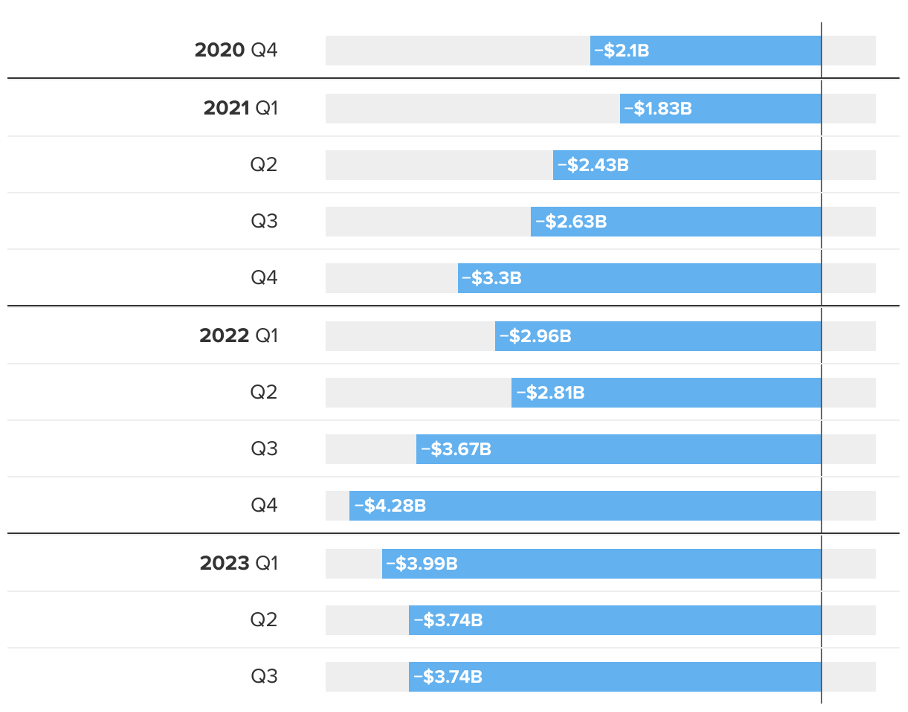

2. Reality Labs spending

Meta’s Reality Labs division reported a $3.74 billion operating loss in its third-quarter earnings report, contributing to cumulative losses exceeding $21 billion since the beginning of last year. Revenue for the virtual reality and augmented reality division declined by 26% to $210 million, falling short of analysts’ expectations of $299.3 million in sales and a $3.9 billion operating loss. While Meta continues to invest billions in VR and AR to advance its vision of the metaverse, the market remains in its early stages. Meta introduced the Quest 3 VR headset in September, emphasizing its technical superiority over the Quest 2 and a more affordable pricing structure, starting at $499. Positioned as a cost-effective alternative to Apple’s (NASDAQ:AAPL) forthcoming Vision Pro mixed reality headset priced at $3,499, Meta aims to make VR more accessible. In June, Meta launched the Meta Quest+ VR subscription service at $7.99 per month, catering to users of Quest 2, Quest Pro, and Quest 3 VR headsets, providing access to two new games monthly.

Meta’s metaverse investments, totaling nearly $50 billion, have yet to yield positive financial results. Despite cost-cutting efforts, Meta anticipates “meaningful” Reality Labs operating losses to rise in 2024. In 2022, Meta’s operating margin dropped from 40% to 25%, with the Reality Labs division’s $13.7 billion operating loss standing out amid a broader decline in Meta’s core business profitability. CEO Mark Zuckerberg defended the long-term vision of the metaverse, emphasizing its historic importance and transformative impact on technology integration in our lives.

3. Competition from TikTok

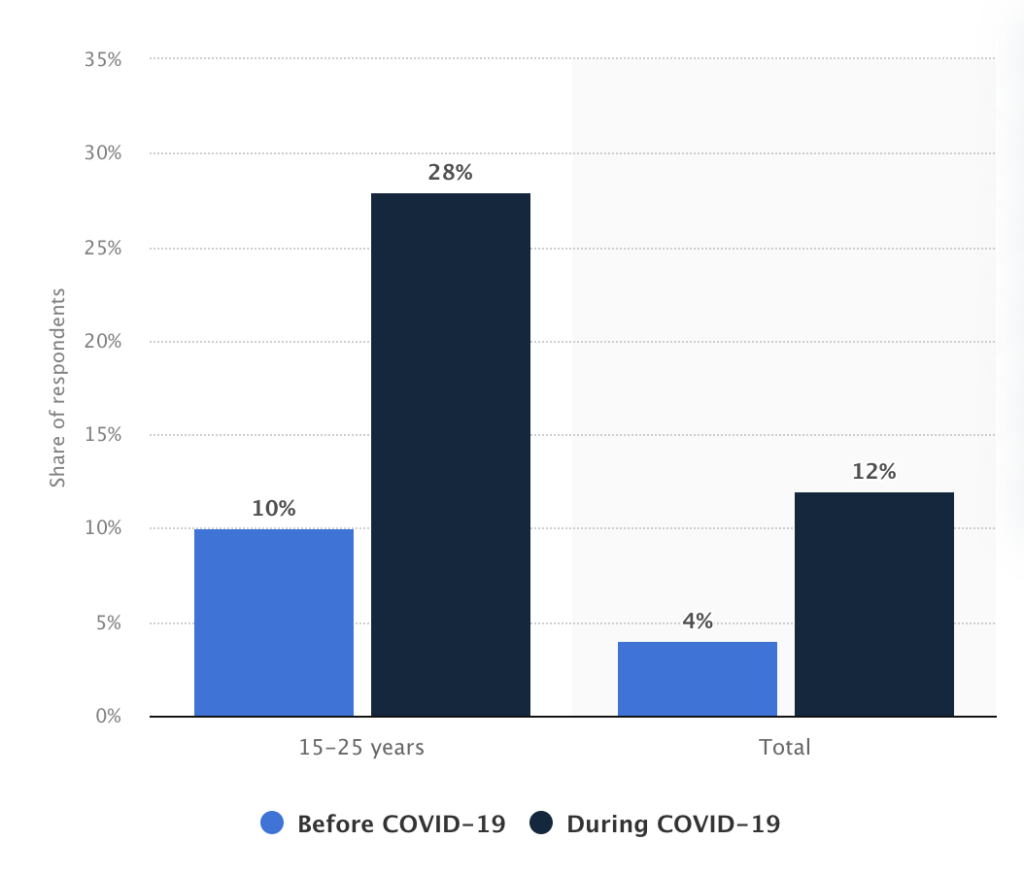

The substantial decline in Meta’s stock can also be attributed to the growing competition posed by TikTok. The TikTok app has been download 4.7 billion times and was the most downloaded app in 2021. The first quarter of 2023 alone witnessed a remarkable 770 million global downloads. The app’s substantial growth can be largely attributed to the surge in user adoption during the COVID-19 pandemic’s early months in 2020, when widespread quarantines prompted increased social media engagement among individuals spending more time at home. According to Statista, TikTok experienced a staggering 180% growth among users aged 15-25 during this period.

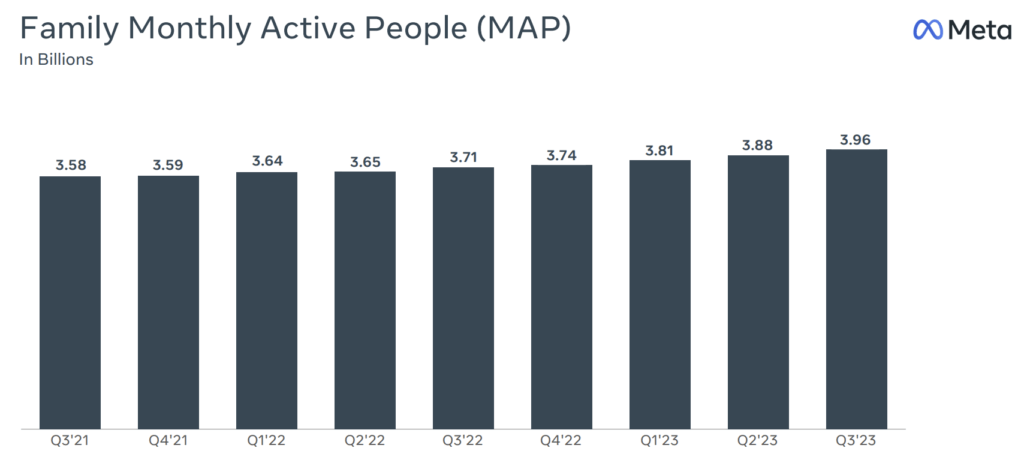

Meta remains the largest social media company with 3.14 billion daily active people (DAP) and 3.96 billion monthly active people (MAP) for their Family of Apps, both an increase of 7% year-over-year. Meta reported its first-ever decline in DAP in Q4 of 2021, losing around 500,000 daily users. The decline in users in Q4 of 2021 and the rising competition from TikTok has had a great impact on Meta’s stock price. Meta has acknowledged TikTok as a competitor, particularly in short-form video content. Meta has even hired a Republican consulting farm, Target Victory, to orchestrate a nationwide campaign against TikTok. Target Victory contracted with numerous PR firms to influence the public opinion against TikTok by placing local news stories and op-eds critical of TikTok. Meta confirmed the hiring, stating that all platforms, including TikTok, should face scrutiny consistent with their success. Targeted Victory’s CEO, Zac Moffatt, emphasized the company’s bipartisan approach on behalf of its clients. The campaign aimed to exploit both genuine concerns and unfounded anxieties about TikTok, using various tactics to turn sentiment against the Chinese-owned platform.

4. Apple’s ad targeting restrictions

Apple (NASDAQ:AAPL) added a feature in April 2021 that marked a significant step in bolstering user privacy. The new feature, included in the iOS 15 operating system update, introduced an App Tracking Transparency (ATT) framework, which mandates user consent for online tracking. These changes presented several new challenges for advertisers, limiting their ability to collect detailed user behavior data for targeted ads and campaign measurement. The implementation of the ATT framework had a significant impact on Meta’s advertising business. Meta estimated that the ATT framework cost Meta around $10 billion in advertising revenue in 2022.

Technical Analysis:

Upon examining Meta’s chart, several key observations come to light. Notably, resistance is identified at the $356 level. Additionally, a discernible upward lower trendline support is evident, potentially poised for a breakout against the backdrop of the prevailing flat resistance. This interplay between resistance and trendline support is identified as the ‘Ascending Triangle Pattern’, where the rising support trendline and flat resistance together create a formation often associated with a possible upward price movement. If Meta manages to surpass this line of resistance, we may witness new highs in 2024.

Financials:

1. Income Statement

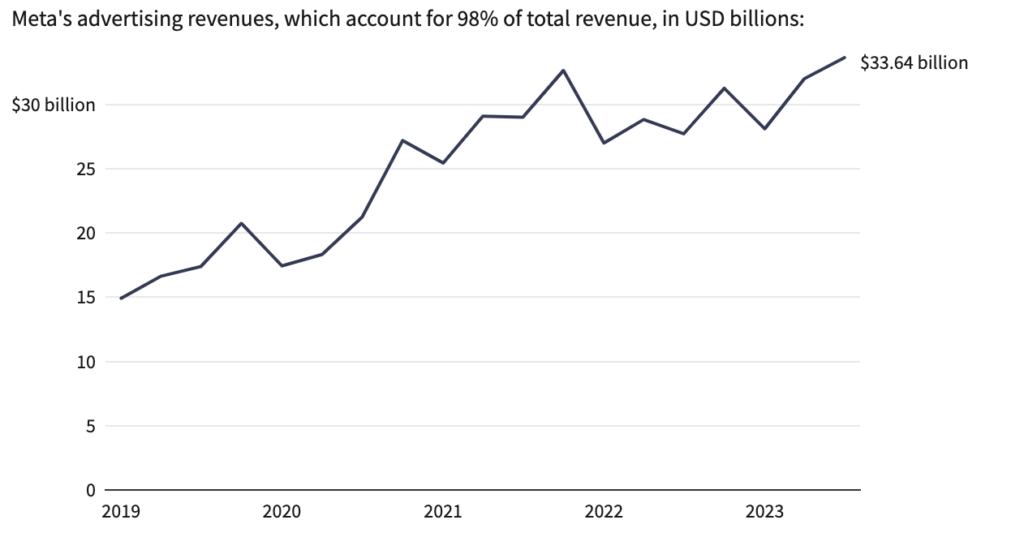

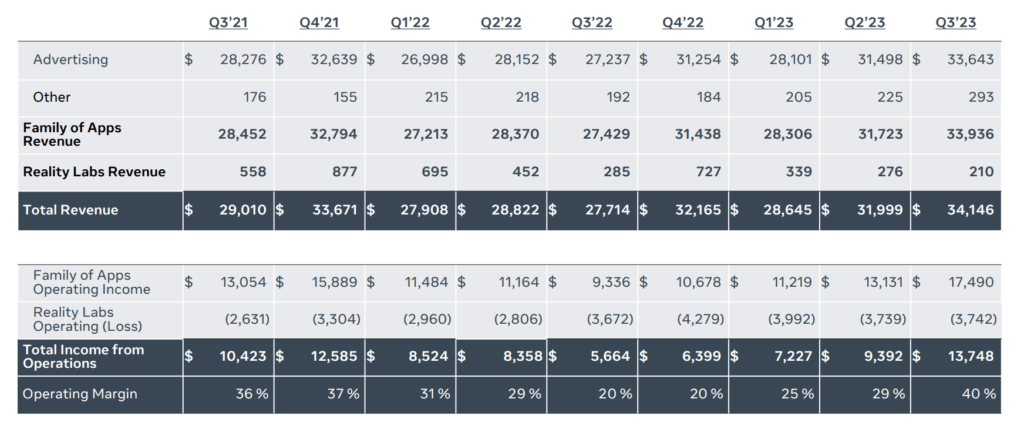

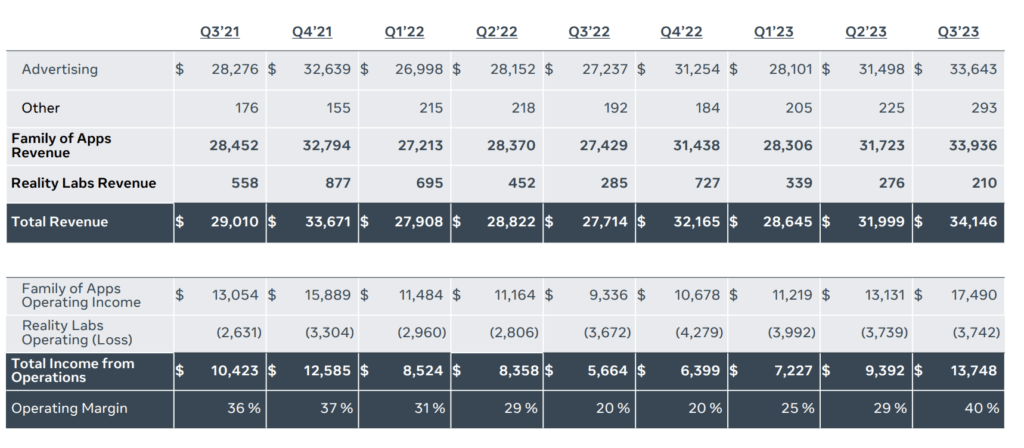

Meta’s Q3 2023 results indicate a revenue of $34.1 billion, aligning with company guidance and reflecting a 23% year-over-year growth. Ad revenue saw a notable 24% increase, reaching a record high of $33.64 billion in Q3 2023. Meta’s Q3 exceeded analysts’ expectations with a net income of $11.6 billion, or $4.39 per diluted share, marking a 164% year-over-year increase. This resurgence in growth marks a recovery from the challenges faced in 2022, including Apple’s ad targeting restrictions, competition from TikTok, and a general slowdown in the ad market, which had impacted Meta’s stock value. Meta’s robust advertising revenue, coupled with ongoing cost-cutting efforts, contributed to these positive results. Consequently, Meta’s stock has rebounded, recouping a substantial portion of its prior losses.

Meta’s operating margin, which stood at 36% in Q3 2021 and 37% in Q4 2021, has declined to as low as 20% in both Q3 2022 and Q4 2022. Fortunately, Meta’s operating margin rebounded in 2023, reaching 40% in Q3 2023. Meta is strategically focusing on monetizing its platforms more effectively. In its Q2 2023 earnings call, Meta revealed that Reels has achieved an annual revenue run rate of $10 billion, showcasing more than triple growth in the past year. Meta is also exploring avenues to enhance monetization for WhatsApp users, introducing paid messaging and business messaging features. Meta anticipates future monetization of Threads, its platform akin to Twitter, introducing a new revenue stream. The combination of heightened monetization efforts and aggressive cost-cutting measures is expected to contribute to a projected 26% year-over-year increase in Meta’s net income for 2024, as forecasted by analysts.

The expansive reach of Meta’s Family of Apps is evident as it attracts approximately 3.96 billion monthly users. Facebook maintains its global growth momentum, boasting 2.09 billion daily active users, a 5% increase from the previous year. The Family of Apps achieved a robust operating income of $17.5 billion, showcasing a notable 52% operating margin. Furthermore, the other revenue segment of the Family of Apps reached $293 million in Q3, marking a substantial 53% growth. This growth was fueled by the remarkable expansion of business messaging revenue through the WhatsApp Business Platform. The latest figures underscore Meta’s continued success and strategic focus on diversified revenue streams within its thriving ecosystem.

Meta anticipates its total revenue for the fourth quarter of 2023 to fall within the range of $36.5 billion to $40 billion. If realized, this would translate to an annual revenue of $131.29 billion to $134.79 billion for the full year of 2023. This implies a revenue growth ranging from 12.59% to 15.59% in 2023.

2. Cash Flow:

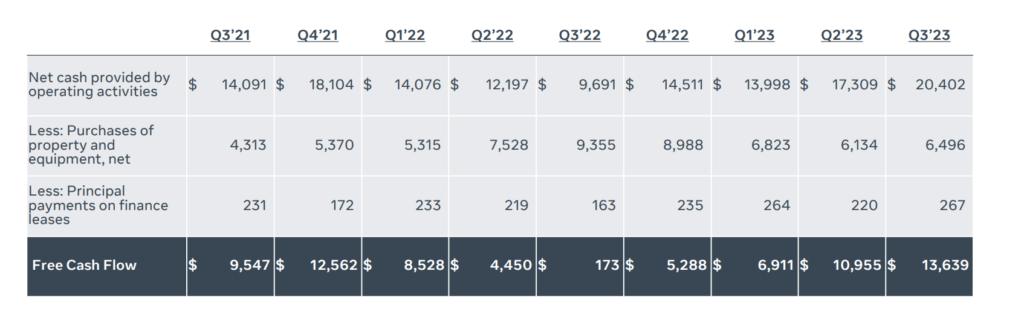

Meta is generating an impressive $13.46 billion in free cash flow, constituting 40% of its $34.1 billion Q3 2023 revenue. The substantial free cash flow was utilized for shareholder-friendly initiatives, including $3.7 billion in share repurchases, leading to a boost in the bank balance and marketable securities by $7.7 billion to over $61.1 billion. With a remarkable 40% free cash flow margin, Meta could potentially surpass its current price. This quarter’s free cash flow marks a significant achievement, representing the highest in recent years for the company.

We can now estimate Meta’s target price. The target price estimation for Meta is based on the assumption of maintaining an average 40% Free Cash Flow (FCF) margin over the next year, meaning that 40% of revenue would convert into free cash flow. We previously projected the annual revenue for 2023 to fall within the range of $131.29 billion to $134.79 billion. Analysts expect the annual revenue in 2024 to rise by 12.8%. Considering this, the average sales for the next 12 months could be approximately $141.5 billion. Assuming a conservative estimate of $55 billion in FCF, a 5% FCF yield valuation (equivalent to a 20x multiple) would indicate a potential market cap of $1.1 trillion (20x $55 billion). As of now, the current market cap stands at $911.86 billion, suggesting a potential increase of over 20.63%. Applying this to the current stock price of $354.83, the target price could reach $428 per share.

Risks:

As previously stated, I will now explore the four factors that contributed to Meta’s stock price decline and explain why these factors no longer present challenges for Meta.

1. Privacy concerns

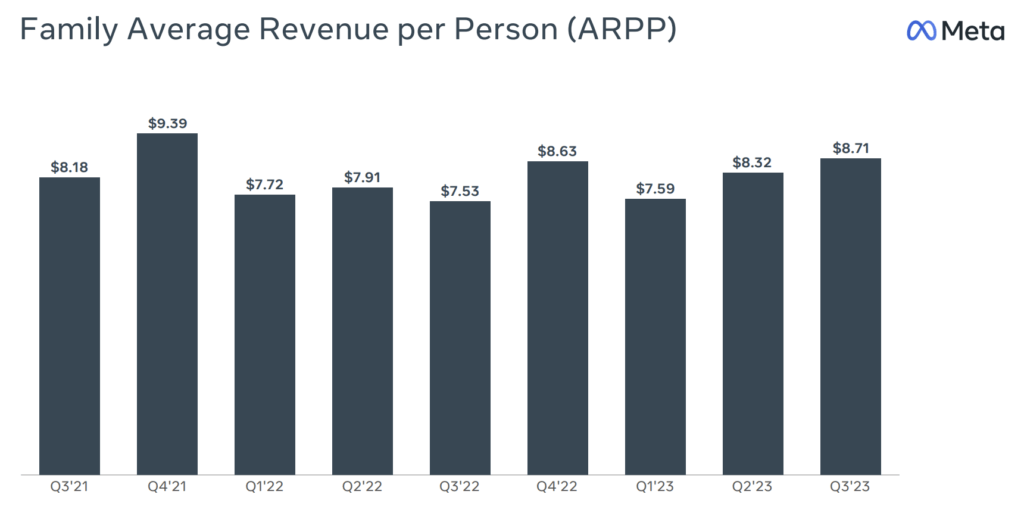

Meta will provide individuals in the European Union (EU), European Economic Area (EEA), and Switzerland with the option to subscribe to a monthly plan for accessing Facebook and Instagram, ad-free. Alternatively, users can opt for the free version, which includes relevant advertisements. Those opting for a monthly subscription won’t have their personal information utilized for targeted advertising. In contrast, users who choose not to pay will still have their data collected to fuel Meta’s profitable advertising model. The subscription for an ad-free experience varies by platform, priced at € 9.99/month on the web and € 12.99/month on iOS and Android. This subscription covers all linked Facebook and Instagram accounts in a user’s Accounts Center until March 1, 2024. After this date, an extra fee of € 6/month on the web and € 8/month on iOS and Android will be charged for each additional account in a user’s Account Center. The pricing on iOS and Android considers fees imposed by Apple and Google. The Family Average Revenue per Person (ARPP) stands at $8.71, signifying that each individual contributes $8.71 to Meta’s earnings.

While Meta cites an EU court ruling affirming a subscription model as “a valid form of consent for an ad-funded service,” privacy activist Max Schrems strongly criticizes this approach, particularly the idea of ending tracking only for paid users. Christophe Carugati, an affiliate fellow at the Bruegel think tank, suggests that Meta’s offer appears to be “fully compliant” with EU rules. However, he notes that the decision on whether online platforms can present users with a binary choice between being tracked or paying for privacy lies with the EU member states. Carugati anticipates that the issue of whether the fee is considered a free choice will be central to any potential legal challenges. There was no immediate comment from the European Commission on whether the subscription option would address privacy concerns in Brussels.

This transition is not a recent development. X, formerly known as Twitter, has already introduced subscription plans. X offers basic, premium, and Premium+ subscriptions, where premium plans entail reduced ads, and Premium+ plans offer an ad-free experience. While I see no immediate legal concerns with Meta’s subscription model and opt-in/opt-out approach, legal disputes over such matters are almost inevitable in the future. Meta is no stranger to legal skirmishes surrounding privacy and data.

2. Reality Labs spending

Meta’s Q3 2023 total expenses were $20.4 billion, down 7% compared to last year. Meta has implemented substantial cost-cutting measures, including multiple rounds of layoffs reducing its headcount by at least 21,000. These actions aim to enhance efficiency and realign business priorities. Within Meta’s Reality Labs segment, Q3 2023 revenue was $210 million, down 26% due primarily to lower Quest 2 sales. Reality Labs expenses were $4.0 billion, flat year-over-year as higher headcount-related expenses were offset by lower non-headcount related operating expenses. Reality Labs operating loss was $3.7 billion.

The struggling division has incurred losses totaling $11.4 billion in the current fiscal year while generating just $825 million in revenue. Meta CFO, Susan Li, stated that Meta expects losses to “increase meaningfully year-over-year due to our ongoing product development efforts in augmented reality/virtual reality and our investments to further scale our ecosystem.” This implies that we should anticipate increased expenditures within Reality Labs in 2024 and the subsequent years.

Reality Labs, despite incurring apparent losses, is positioned as a long-term investment for Meta. The majority of its spending is directed toward research and development. While 2024 is expected to see continued losses due to ongoing product development, Meta’s overall financial performance remains strong. The future of Reality Labs appears promising, showcasing Meta’s dedication to pioneering AR and VR technologies for a digital future. I have consistently emphasized that gaming will be the primary driver for the widespread adoption of the metaverse, VR, and AR technologies. I view Microsoft’s introduction of the Xbox Game Pass to Meta Quest 2, 3, and Pro headsets as a positive development. Subscribers can now stream numerous games to their VR headsets through the Xbox Cloud Gaming beta app, with gameplay requiring a Bluetooth controller. Furthermore, I anticipate that the introduction of Apple’s AR/VR headset will have a considerable impact on the entire industry, potentially providing a boost to overall sales. This expectation is grounded in the notion that Meta’s existing headsets are competitively priced, making them more accessible to a broader consumer base. As Apple enters this market, the increased competition and heightened consumer interest in AR/VR experiences may lead to an overall expansion in the market, benefiting both Meta and Apple, as well as driving innovation within the industry.

3. Competition from TikTok

Meta responded swiftly to TikTok’s short video format by leveraging Instagram Reels. As mentioned by Mark Zuckerberg during Meta’s Q3 2023 earnings call, Reels has driven more than 40% increase in time spent on Instagram since their launch. Moreover, Meta has also reached a monetization milestone earlier than expected and Meta estimates that Reels is now net neutral to overall company ad revenue. Reels has evolved from an early initiative to a core component of Meta’s apps. Looking ahead, Meta aims to nurture the growth of Reels and integrate it seamlessly into a broader portfolio of video services, which collectively captures over half of the user engagement on Facebook and Instagram. The potential for expansion and innovation within this domain is substantial. I think we should acknowledge what Meta does best: copy working strategies and adapt them effectively to stay competitive in the ever-evolving social media landscape.

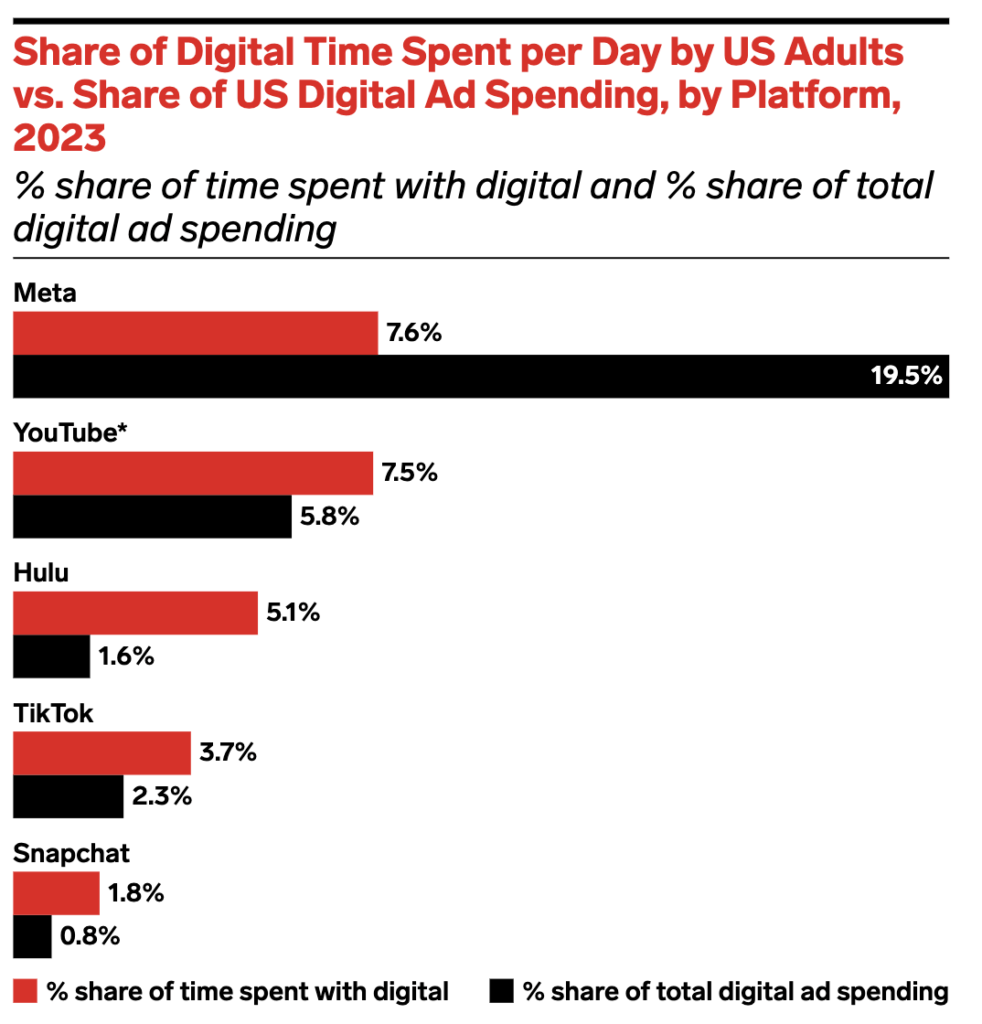

Meta is acknowledged as one of the two most prominent players in digital advertising, alongside its rival Google (NASDAQ:GOOGL). However, Meta’s ad dominance does not align proportionally with consumers’ time spent on its platforms, a notable deviation compared to competitors such as YouTube and TikTok. This year, the US adult population was expected to spend slightly over 34 minutes per day on Meta apps, constituting approximately 41.8% of daily social media time and 7.6% of overall digital media time. Despite this, Meta is projected to command around 75% of social ad dollars and nearly 20% of total US digital ad spending. In comparison, YouTube’s time spent figures also average around 34 minutes per day. Despite claiming 7.5% of adults’ digital media time, YouTube is set to attract only 5.8% (gross) of all digital ad spending.

Meta defies expectations by achieving remarkable monetization results compared to the time users spend on its platforms. While other major rivals, such as Google (NASDAQ:GOOGL) and Amazon (NASDAQ:AMZN), focus more on clicks than user engagement, social networks and digital video platforms rely on prolonged user attention for success. Meta appears to have mastered the art of translating user engagement into substantial monetization, a feat unmatched by its counterparts. TikTok shows promise but has a considerable journey ahead. The platform’s ad revenue growth is anticipated to far exceed its time spent growth in the coming years, gradually improving its ratio on the chart. Other platforms may experience similar trends, albeit to a lesser extent, but TikTok’s rapid ad business growth positions it as the only contender with the potential to eventually outperform time spent, echoing Meta’s success. However, achieving this milestone remains a distant prospect, contingent on factors like potential US bans.

TikTok has over 1.7 billion users globally, out of which 1.1 billion are its monthly active users. In Q3 2023, Meta’s Monthly Active People (MAP) reached 3.96 billion, a remarkable figure given the global population of 8 billion. Meta’s unparalleled audience scale further solidifies its dominance in the social media domain, providing a foundation for the creation of new platforms like Threads. Threads currently has 141 million users and reached 70 million users in two days. This milestone was achieved without adoption in European Union due to privacy concerns. Meta can leverage its vast global user base to integrate it into the metaverse and other products and services.

4. Apple’s ad targeting restrictions

Meta’s exceptional ability to generate ad revenues disproportionate to user engagement underscores the company’s historical prowess in technology and operations. While Apple’s ATT framework introduced disruptions, Meta has largely cracked the code in terms of leveraging user data, streamlining ad placements, facilitating marketer operations, and ensuring measurable return on investment. This is further evidenced by the restoration of Meta’s operating margin to 40%. It appears that Apple’s ATT framework is no longer a hindrance.

Conclusion:

Meta Platforms has seen a remarkable 187.73% YTD surge, recovering from a low of $90 in 2022. Key factors impacting Meta’s performance include privacy concerns, substantial Reality Labs spending, competition from TikTok and Apple’s ad targeting restrictions. Despite challenges, Meta has demonstrated financial resilience with robust revenue and aggressive cost-cutting. Technical analysis suggests a potential upward price movement. Future projections indicate a 26% YoY increase in net income for 2024. User metrics remain strong with billions of daily and monthly active users. Meta’s strategic investments in VR, AR, and enhanced monetization efforts position it for growth. Despite potential legal disputes and ongoing losses in Reality Labs, Meta’s resilience and adaptability suggest a positive outlook, with a target price potentially reaching $428 per share in 2024.

Great insights!!

Thank you!

Wow! Love your analysis!!! Can’t wait to read more